Lasso and ridge regression are two alternatives – or should I say complements – to ordinary least squares (OLS). They both start with the standard OLS form and add a penalty for model complexity. The only difference between the two methods is the form of the penality term. Ridge regression uses the

Ridge Regression:

Lasso Regression:

Ridge regression has a closed form solution that is quite similar to that of OLS:

In ridge regreession when

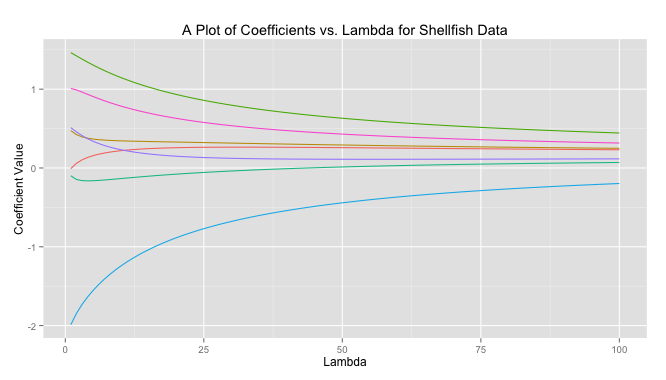

The code to produce this graph is quite simple.

# Load libraries library(MASS) library(reshape) library(psych) library(ggplot2) # Get data data read.csv(file = "Masked") # Prepare data X data[,-10] X scale(X, center = TRUE, scale = TRUE) response data[,10] response scale(reponse, center = TRUE, scale = FALSE) # Get ridge solution for every lambda betas matrix(rep(NA), nrow = 7, ncol = 100) rownames(betas) colnames(X) lambda 1:100 betas lapply(1:length(lambda), FUN = function(i) { return(solve(t(X)%*%X + diag(x = lambda[i], ncol(X)) )%*%t(X)%*%response) }) # Prepare data for plot betas data.frame(t(betas)) betas cbind(lambda, betas) betas (betas, id = "lambda", variable_name = "coviariate") # Plot ggplot(betas, aes(lambda, value)) + geom_line(aes(colour = coviariate)) + ggtitle("A Plot of Coefficients vs. Lambda for Shellfish Data") + xlab("Lambda") + ylab("Coefficient Value") + theme(legend.position = "none")

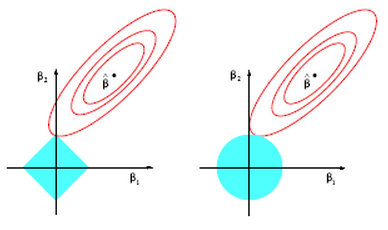

Lasso on the other hand does not have a closed form solution so numerical techniques are required. The benefit of lasso, however, is that coefficients are driven to exactly zero. In this way lasso acts as a sort of model selection process. The reason ridge regression solutions do not hit exactly zero, but lasso solutions do is because of the differing nature of the geometry of the

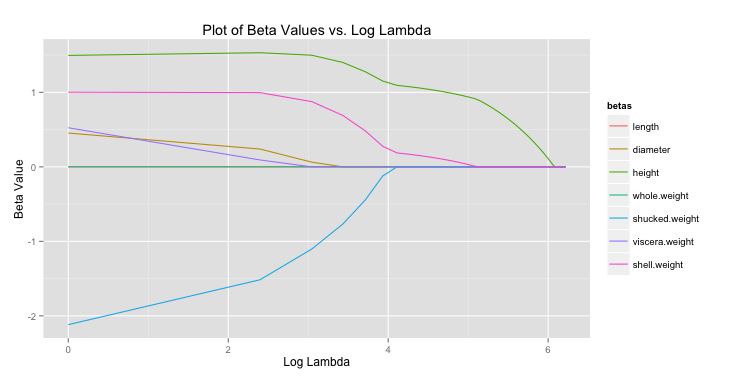

For lasso regression, then, solutions end up looking like the graph below. As

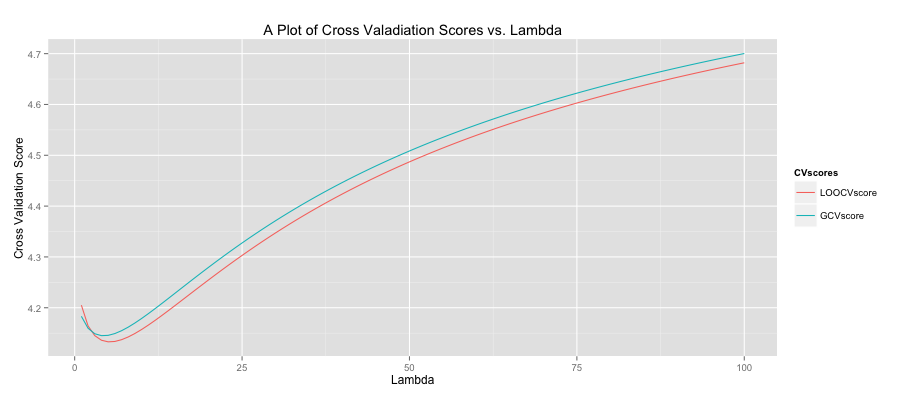

All of this begs the question, “what lambda values is ideal?” To determine this cross validation (CV) is often used. For each

The code to produce this graph is shown below.

# Get data data read.csv(file = "Masked") # Prepare data X data[,-10] X scale(X, center = TRUE, scale = TRUE) response data[,10] response scale(response, center = TRUE, scale = FALSE) lambdaSeq 1:100 LOOCVscore rep(0, length(lambdaSeq)) GCVscore rep(0, length(lambdaSeq)) # Get leave-one-out CV score LOOCVscore lapply(lambdaSeq, FUN = function(i) { lambda [i] hat = X %*% (solve(t(X) %*% X + lambda*diag(ncol(X))) %*% t(X)) prediction = hat %*% response Lii = diag(hat) return(mean(((response - prediction)/ (1 - Lii))^2)) }) # Get GCV score GCVscore lapply(lambdaSeq, FUN = function(i) { lambda [i] hat = X %*% (solve(t(X) %*% X + lambda*diag(ncol(X))) %*% t(X)) prediction = hat %*% response Lii = tr(hat)/nrow(X) return(mean(((response - prediction)/ (1 - Lii))^2)) }) CV as.data.frame(cbind(lambdaSeq, LOOCVscore, GCVscore)) CV (CV, id = "lambdaSeq", variable_name = "CVscores") ggplot(CV, aes(lambdaSeq, value)) + geom_line(aes(colour = CVscores)) + ggtitle("A Plot of Cross Valadiation Scores vs. Lambda") + xlab("Lambda") + ylab("Cross Validation Score")

Created by Pretty R at inside-R.org

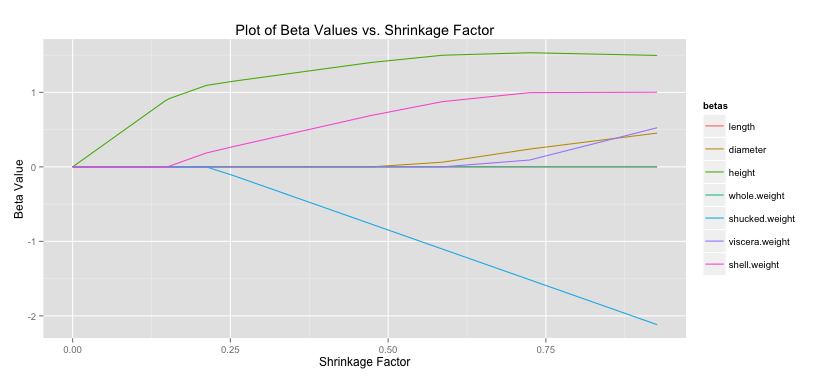

Another common statistic often presented when doing lasso regression is the shrinkage factor, which is just the ratio of the sum of the absolute value of the coefficients for the lasso solution divided by that same measure for the OLS solution. Remember small

As I mentioned there is no closed-form solution that can determine the coefficients in the case of lasso regression. There are a number of methods to search through and find these betas, however. Luckily, minimizing the lasso solution results in a convex optimization problem so given enough iterations we can converge very close to the global solution. The method presented below is my implementation of the shooting algorithm. The shooting algorithm is stochastic: it picks a random beta, removes it from the model, calculates the effect of this deletion, and assigns the left out beta a value proportional to this effect, which is based on a formula I won’t present here. We were meant to determine our own criteria for stopping the loop (you could theoretically repeat this process forever). I choose a method that makes sure all betas have been updated and then calculates the MSE of the current model. If it’s within some tolerance – playing around the number suggested .001 was pretty good – the loop stops and we move on to the next lambda value. Otherwise we must continue iterating until all betas have been updated once more and the tolerance check repeats.

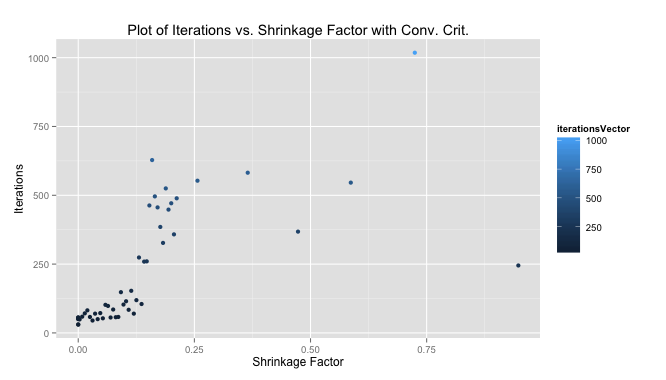

We were told to plot our iterations as a function of the shrinkage factor. The performance using my convergence criteria was much better than with the 1,000 iterations we were told to start with as a test case. The median number of iterations for my solution to converge quite close to the 1,000-iteration method was 103, meaning my algorithm improved performance by 10 times (at least measured by iterations).

# Read in data data read.csv(file = "Masked") # Perpare data X as.matrix(data[,-10]) X scale(X, center = TRUE, scale = TRUE) response data[,10] response scale(response, center = TRUE, scale = FALSE) # Initialize variables set.seed(35) lambdaSeq seq(from = 1, to = 501, by = 10) betaVectorConv matrix(NA, ncol = 7, nrow = length(lambdaSeq)) iterationsVector rep(NA, length(lambdaSeq)) aj 2*colSums(X^2)[1] # Get lasso solution using shooting algorithm for each lambda for(i in 1:length(lambdaSeq)) { lambda [i] betas solve(t(X) %*% X) %*% t(X) %*% response betaUpdate rep(NA,7) exit = FALSE iterations 0 MSECurrent 0 MSEPast 0 while(exit == FALSE) { j sample(1:7,1) betaUpdate[j] 1 iterations 1 xMinJ [,-j] betaMinJ [-j] xj [,j] cj 2*(t(xj) %*% (response - xMinJ %*% betaMinJ)) if(cj < -lambda) { betas[j] (cj + lambda)/aj } else if(cj > lambda) { betas[j] (cj - lambda)/aj } else { betas[j] 0 } if(sum(is.na(betaUpdate)) == 0) { yHat sum((response - yHat)^2) if(abs(MSECurrent - MSEPast) < .001) { iterationsVector[i] TRUE } MSEPast rep(NA,7) } } betaVectorConv[i,] } #Calculate shrinkage colnames(betaVector) colnames(X) betaLS solve(t(X) %*% X) %*% t(X) %*% response betaLS sum(abs(betaLS)) betaLasso abs(betaVectorConv) betaLasso apply(betaLasso,1,sum) betaShrink # Prepare shrinkage data for plot betaShrinkPlot as.data.frame(cbind(betaShrink,betaVector)) betaShrinkPlot (betaShrinkPlot, id ="betaShrink", variable_name = "betas") # Plot shrinkage ggplot(betaShrinkPlot, aes(betaShrink, value)) + geom_line(aes(colour = betas)) + ggtitle("Plot of Beta Values vs. Shrinkage Factor with Conv. Crit.") + xlab("Shrinkage Factor") + ylab("Beta Value") # Prepare and plot iterations betaIterPlot as.data.frame(cbind(betaShrink, iterationsVector)) ggplot(betaIterPlot, aes(betaShrink, iterationsVector)) + geom_point(aes(colour = iterationsVector)) + ggtitle("Plot of Iterations vs. Shrinkage Factor with Conv. Crit.") + xlab("Shrinkage Factor") + ylab("Iterations")

One thought on “Lasso and Ridge Regression in R”